Real default is knocking louder and louder on the American door

Read Time:9 Minute, 51 Second

On May 2, just before the key rate was raised to 5.25%, the U.S. Department of the Treasury sounded the alarm because the U.S. government had only one month of available funds to cover its budgetary obligations. Due to a slowing U.S. economy tax revenues were weak in April. Republicans in Congress passed their own budget bill that cuts government spending by $100 billion and freezes green energy subsidies and tranches to other countries. They were demanding the White House to accept this version of the budget, albeit with some compromises, but Biden had long refused to enter into any negotiations with Congress, accusing the Republicans of holding the whole of America hostage by their unwillingness to raise the national debt ceiling from January.

However, time was running out, and by mid-May the first meeting between Biden and McCarthy in three months was scheduled. The U.S. financial authorities, for their part, feared that as the date of default approached, America could face a credit rating downgrade. This already happened in 2011 when the U.S. was downgraded from AAA to AA+ amid another round of confrontation between Congress and the White House. Since then, the rift in America has only intensified, and Washington was at a very real risk of a technical default last months. The consequences for the U.S. economy would be catastrophic with a falling dollar and a guaranteed recession. Therefore Congress and the White House were forced to find compromise at the last moment. But even in this case, turbulence in the markets was not avoided, as well as a drop in demand for U.S. Treasury bonds, in connection with which to service the national debt in the future will be even more difficult than today.

Another Fed rate hike also dealt a blow to the stability of financial markets. However, explaining its decision, the Federal Reserve hinted that the current increase could be the last one. After all, now the situation is already at risk of becoming unmanageable largely because of this growth, since the beginning of the year four American banks have already collapsed, and at least several are in line for bankruptcy. The level of dollar inflation, which the Fed has been fighting so vigorously, has recently fallen to 5%. That’s still a lot, but a lot less than last year’s 8-9%. Now the U.S. economy is threatened by something else entirely: growth is slowing, and the risks of a recession are becoming very real. However, “low” inflation is an achievement of the Biden government, which is why he is not particularly eager to abandon “successful” monetary measures. In addition, the mortgage market is experiencing serious instability, and in many cities, home values have already plummeted by 10-15% over the year. The debt crisis is worsening, and the number of small business bankruptcies has jumped to its highest level since the beginning of the pandemic. Raising money at the current inflated rates is becoming more and more problematic for municipalities and states, as well as for large corporations. A wave of numerous layoffs and staff reductions is also gaining momentum. In fact, this monetary policy is causing problems for the U.S. government as well. After all, this year due to rising rates the government will have to spend up to $1.5 trillion to service the national debt, which is 20% of the budget. The interest on treasury securities has also soared because of the threat of a technical default. It is obvious that the moment is approaching when we have to zero rates and turn on the printing press again, even if it leads to a jump in inflation, or a new crisis cannot be avoided. After all, with the Republicans in a tough position, the only salvation for the Biden administration is unfunded issuance.

Against this background, experts in Washington analyzed the consequences of the budget crisis for the United States. They forecasted three scenarios. The first scenario was like this: Congress and the White House would stall and agree on a new budget shortly before a possible default. This would threaten to lower the credit rating of the U.S. and deprive the economy of 300,000 jobs and 0.3% of GDP growth. The second scenario was: America announced a technical default, but only for a couple of days. The impact would be primarily reputational. Washington’s status as a reliable borrower would suffer, as well as the processes of de-dollarization would be accelerated. In this case, the Fed would quickly release billions of dollars into the debt market and begin to buy U.S. Treasury bonds that had been defaulted on. This would soften the blow of a default, but even in this situation the U.S. would be in danger of losing half a million jobs. The third and worst scenario was: the default situation would drag on for weeks and months. The U.S. was then guaranteed to slide into a new recession worse than it was in 2008 or during the COVID-19 pandemic. The dollar would fall sharply, stock markets would plummet 45%, and the U.S. would lose 8 million jobs. Millions of welfare recipients and government workers would lose their payments. Tens of thousands of soldiers at 700 U.S. bases around the world would also be in limbo, losing their Pentagon funding. Such a default scenario would not only cause a global crisis, but also would bring down the U.S. position as a superpower. It was unlikely that Washington would come to this, and the most probable was the first scenario, when at the very last moment it would have to find a budget compromise and reduce the government spending. And as you know it happened so in the beginning of June.

The debt crisis in the U.S. is increasingly worrying among its allies in Europe and Asia as well. And it’s not just the long inability to raise the national debt ceiling, but also its accelerating volume, which is being spent on useless purposes. Over the past 30 years, the U.S. national debt has jumped tenfold from $3 trillion to $30 trillion. And that’s twice as fast as the country’s economic growth. Since the beginning of Obama’s presidency, the national debt has tripled, and in 2023 it will take a quarter of the U.S. budget to service it. In the next 10 years, the national debt could reach $50 trillion if it is not stopped. To spend on interest payments will be up to half of the entire budget, and this is the level of many Latin American countries, living from default to default. Fears of an uncontrolled surge in national debt are what led to the current budget war in Washington. After all, Congress demanded to first cut government spending and only then raise the debt ceiling. The White House planed to deal with the national debt without the participation of Congress, arguing that under the U.S. Constitution the President has this right. However, this is highly questionable. Even if a short-term solution satisfactory to all will be found, even in the best-case scenario government spending can be reduced by only a few tens of billions of dollars, which is a drop in the ocean against a budget deficit of $2 trillion. By the early 2030s, the budget deficit risks reaching 8-10% of GDP, and the social welfare system will be on the verge of bankruptcy, and that is when the U.S. will face not a technical default, but a very real one.

But, as always, the U.S. financial authorities keep hoping that they will be able to pass the year 2023 without falling into a new crisis and recession. Although the problems in the U.S. economy continue to worsen, and this summer the U.S. promises a whole set of climatic anomalies. Besides, in May the Republicans in Congress outlined their “red line” and said they wanted to cut government spending by at least $130 billion this year. But the White House found itself going for it, because it would have put important “green” subsidies and international programs of the State Department under the knife. Washington continued to pin its hopes on a “soft landing” scenario for the economy, with falling inflation but no recession. However, imbalances in the U.S. economy are appearing more and more. If the recession does not start this year, but next year, it threatens to bury Biden’s chances of re-election, and will contribute to Trump’s return to power. Realizing this, the U.S. president went to negotiate with Republicans, but his meeting with congressional leaders ended up with nothing.

On May 10 they failed to reach an agreement on resolving the budget crisis in the U.S. and raising the debt ceiling and the culprit for the failure was Biden. He showed rare stubbornness and refused to go along with any cuts in government spending. Republicans demanded a revision of the US budget policy, pointing to the simple fact that the budget deficit in 2023 will reach a record $2 trillion, which is 8% of the country’s economy. Rates on U.S. Treasury bonds, which expired in early June, soared to a record 5.5% since 2000. Investors were buying up default insurance in droves, fearing that this worst-case scenario cannot be avoided. Meanwhile, in reality, Biden’s team portrays that all is well in the country and even refused to cancel Biden’s upcoming trips to Australia, Japan and Papua New Guinea, where the U.S. is trying to contain China’s growing influence. The situation was also complicated by the fact that no one knew exactly when the U.S. Treasury would run out of money.

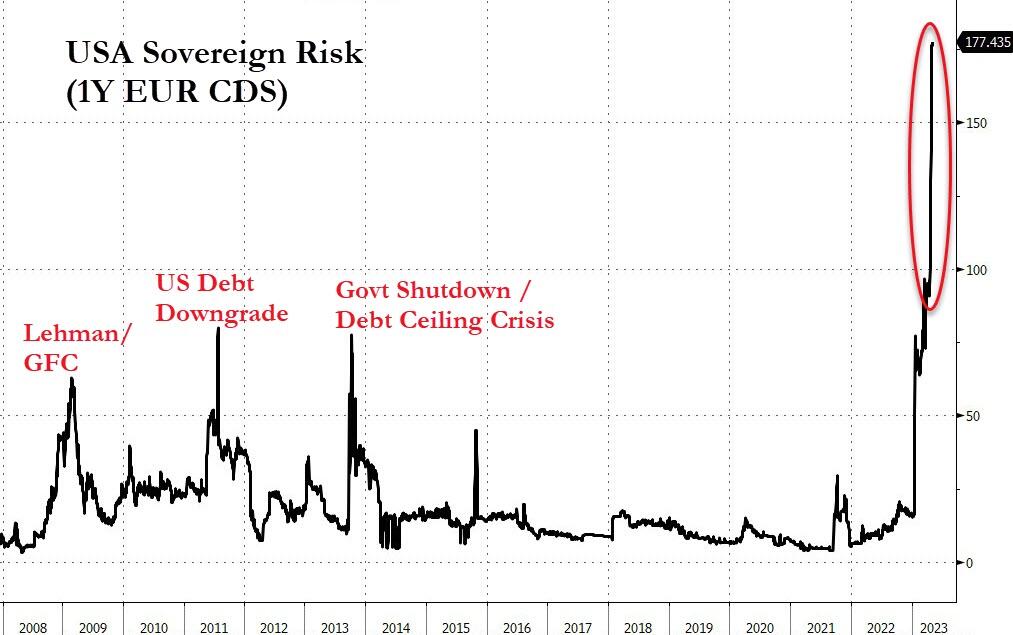

All this is causing great pessimism among financial institutions, and the cost of U.S. default insurance has jumped to an all-time high. It is now even more popular than default insurance for Greece, Brazil or Mexico, which traditionally have many financial problems. Banks and hedge funds on Wall Street, which invested trillions of dollars in U.S. bonds, are massively insured against default, because otherwise they would face catastrophic losses. But in the event of a U.S. default, holders of insurance can expect huge profits of up to 2400% of their investments. Of course, if the financial system does not collapse by then and they are paid off. Indicatively, Moody’s raised the probability of default to 10%, and threatened to lower the U.S. credit rating. In the event of a default, the first states to be hit were those where military and aerospace production, which depends on public money, is concentrated. First of all there will be states like Florida, Ohio, Pennsylvania, Virginia, Kansas and Washington. When it comes to the reaction of ordinary citizens, American society still remains divided on the issue of default. Most Democrats are demanding that the U.S. budget crisis be resolved as soon as possible. But the bulk of Republicans believe that it is possible not to raise the debt ceiling at all, because government spending and the budget deficit are growing at an unacceptable rate, and servicing the national debt under such conditions will be more and more problematic. Not surprisingly, Biden calls a U.S. default a disaster for the whole world, while Trump admits the possibility of default, which is much better for him than an endless build-up of debt. It is this political split that is the root cause of the current budget crisis, which has put America at risk of default, recession and a dramatic weakening of its position in the world. Very soon we will find out where it will lead.

Happy

0 %

Sad

0 %

Excited

100 %

Sleepy

0 %

Angry

0 %

Surprise

0 %

{kind=link}

Average Rating